As investors open their April statements, they might be disappointed to see another month of losses. There have been few places to hide during this current market downturn.

The stock market, as represented by the S&P 500 Index, lost nearly 9% in April and is down almost 13% year to date. The bond market, which can often be a safe haven for investors during a stock market downturn, also lost nearly 4% in April and is down 9.5% year to date as represented by the Bloomberg US Aggregate Bond Index.

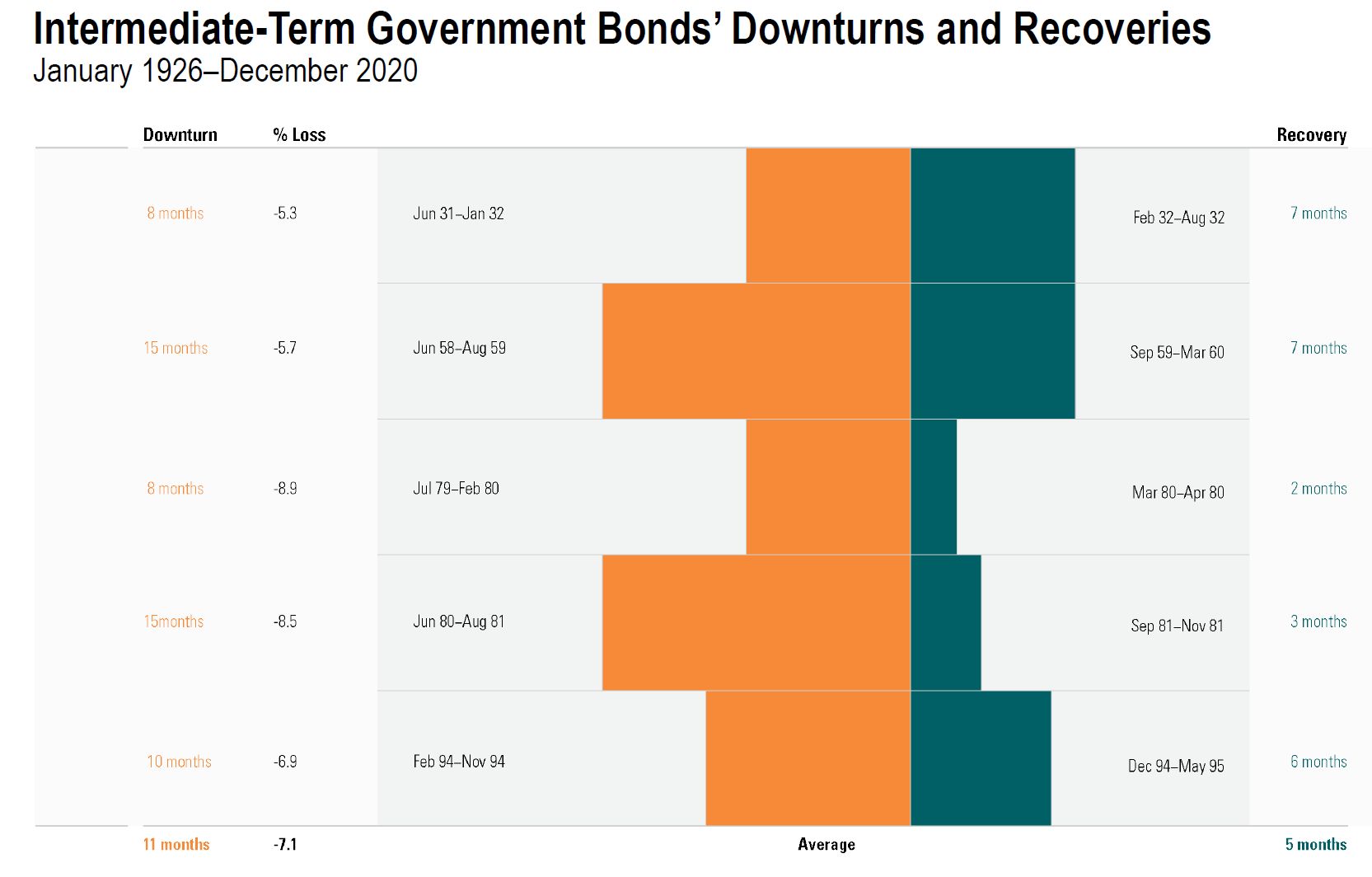

This historically has been a bad few months for bonds, with corporate bonds experiencing their worst performance since 1980 and U.S. Treasury bonds having their worst performance since 1926, according to information from the !

Rapidly rising inflation and interest rates are to blame as bond prices fall when interest rates rise. Stock investors are used to this level of volatility but it comes as a surprise to most bond investors. According to Morningstar, intermediate-term Treasury bonds have fallen over 5% only five times since 1926. The good news is that it took an average of only five months for the bond market to recover its value after those drops.

A five-year Treasury bond offered an interest rate of about 1.3% at the start of 2022 and that rate has now risen to close to 3% according to the . Bond investors will eventually benefit from these higher interest rates as their current bonds mature and they can purchase new bonds offering the higher interest.

Another unusual occurrence that has grabbed news headlines is that the yield curve has “inverted.” This technically means that shorter-term bond rates (2-year Treasuries) have risen above longer-term bond rates (10-year Treasuries). It can be interpreted that while shorter-term rates are rising to combat inflation, investors believe that rates will decline in the future to combat a slowing economy.

It garners a lot of attention because most of the time when the yield curve inverts, a recession follows. However, the predictability of the time until a recession is very imprecise. Over the past six recessions, the lag time between an inversion and a recession has ranged from as little as six months to as long as three years, according to Morningstar. In fact, the S&P 500 stock index has gained 29% on average and peaked nearly 17 months later after the previous four inversions according to LPL Research. In summary, a yield curve inversion can be a warning sign for a recession but it does not mean that trouble is coming immediately.

Deutsche Bank spooked investors in April by becoming the first major bank to forecast a recession in the U.S. However, they predict that recession will come in late 2023 or early 2024. Also, 75 economists surveyed by the in April put the probability of a recession occurring over the next 12 months at only 28%.

A lot of positives in the economy still exist with unemployment below 4%, consumer spending increasing with trillions of savings built up during the pandemic, and nearly 80% of companies still beating earnings expectations with profits at close to 70-year highs, according to FactSet.

We feel that our investment team has prepared our clients’ portfolios for market volatility. We have tried to keep the average maturity of our bond portfolios relatively short as we anticipated that interest rates would be rising. This has helped reduce losses and should help our bond accounts recover faster. We also believe that the majority of anticipated interest rate hikes from the Federal Reserve are already reflected in bond prices so we feel it should begin recovering soon.

We have also been investing in more higher quality “value” stocks with lower prices relative to their earnings or assets. This has been beneficial as value stocks have lost 5% this year but “growth” stocks that favor more technology companies have lost 20% (based on the S&P 500 Value and Growth Indexes).

We also try to be proactive by building up cash in client accounts to provide 12 months’ worth of withdrawals so they are not forced to sell during a market downturn.

We understand that coping with market drops can be stressful. But long-term investors are typically rewarded by sticking with their investment plan. Thank you for your continued trust and please reach out to your financial planning team at 515-225-6000 with any questions regarding your investments.